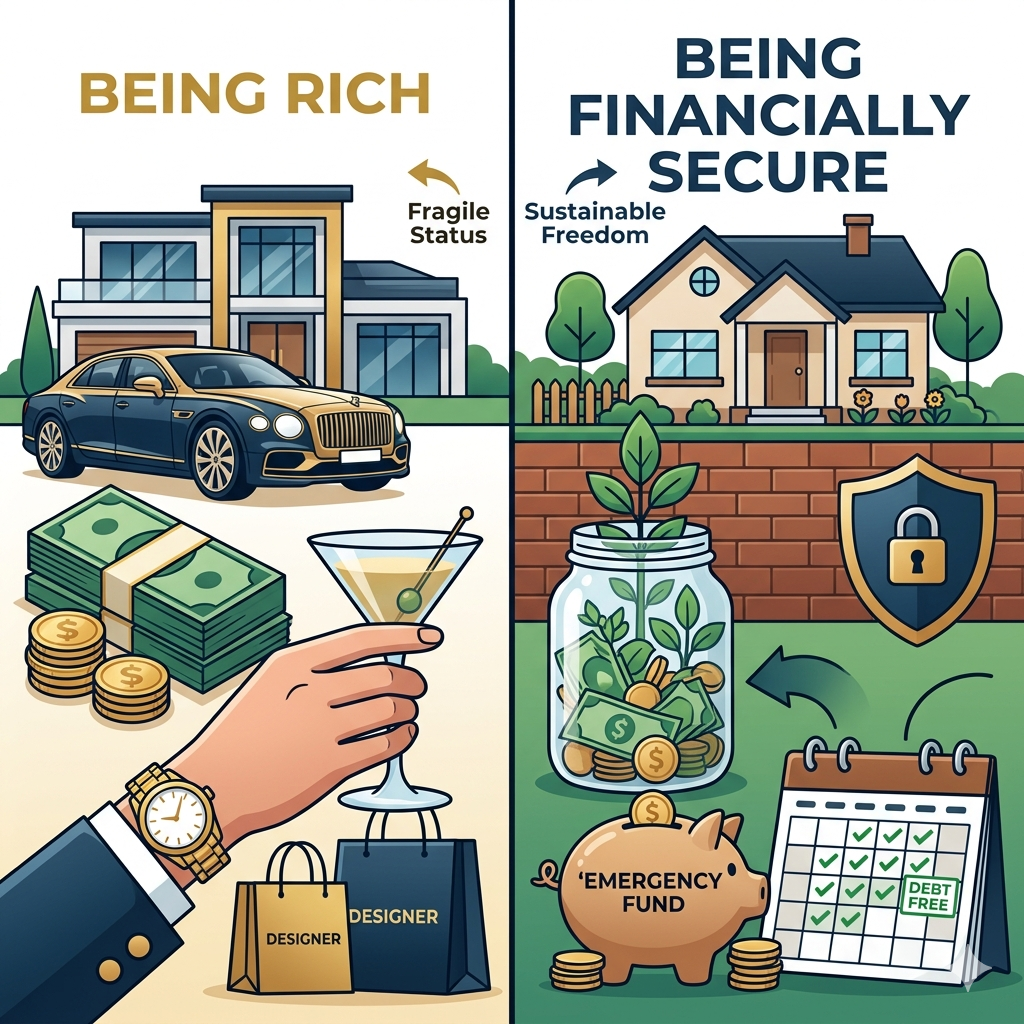

When we think about financial success, most of us picture a lifestyle defined by luxury: high-end cars, designer wardrobes, and expansive homes. We use the word “rich” as a catch-all term for anyone who seems to have an abundance of money. However, there is a profound structural and psychological gap when comparing financial security vs being rich. While “being rich” is often a snapshot of someone’s current cash flow or visible spending, “being financially secure” is a long-term state of resilience and freedom. Understanding this distinction is not just a matter of semantics; it is the difference between living a life of high-stress performance and one of deep-seated peace.

Introduction: Why We Confuse Financial Security vs Rich

In our modern, social-media-driven culture, the lines between financial security and being rich have become increasingly blurred. We are constantly bombarded with images of “rich” lifestyles that suggest success is measured by what you consume. However, many people who appear rich are actually one or two missed paychecks away from a total financial collapse. This is because “richness” is often fueled by high income that is immediately offset by high expenses—a phenomenon known as lifestyle inflation.

On the other hand, financial security is frequently invisible. It is the quiet confidence of knowing that if your primary source of income disappeared tomorrow, your life wouldn’t fall apart. It is about building a “financial fortress” that protects you from the volatility of the economy, job markets, or even your own investment risks. By shifting your focus from looking rich to becoming secure, you move from a fragile existence to a robust one.

“Wealth is the ability to fully experience life.” — Henry David Thoreau

Key Differences at a Glance: Financial Security vs Wealth

To help visualize how these two concepts diverge in daily life, consider the following comparison:

| Feature | Being “Rich” (Status Focus) | Being “Financially Secure” (Safety Focus) |

| Visibility | High (Flashy cars, big houses, luxury goods) | Low (Savings, insurance, quiet investments) |

| Sustainability | Fragile (Depends entirely on high current income) | Resilient (Depends on assets and low overhead) |

| Primary Driver | Social validation and consumption | Freedom and peace of mind |

| Debt Level | Often high (Leveraged to maintain an image) | Low to zero (Avoids high-interest obligations) |

| Reaction to Crisis | High stress/Panic (No margin for error) | Calculated/Calm (Has an emergency buffer) |

What Does Being “Rich” Actually Mean?

To truly understand the difference between being rich and being financially secure, we first have to strip away the Hollywood version of “rich.” In professional financial terms, being rich is almost entirely defined by current cash flow and conspicuous consumption. It is a state of having a high volume of money passing through your hands at any given time. However, the fatal flaw in focusing solely on being rich is that it is often a “high-maintenance” state. To remain rich, you must continuously generate high levels of income because your lifestyle expenses are usually scaled to match (or even exceed) your earnings. This creates a precarious cycle where the individual is essentially running on a financial treadmill: the moment they stop running, the “rich” lifestyle disappears.

One of the most dangerous traps people fall into when pursuing wealth vs. financial security is the Income Trap. We often assume that someone earning $500,000 a year is automatically better off than someone earning $75,000. But if that high earner spends $490,000 to maintain their status—covering luxury car leases, high-interest jumbo mortgages, and elite social club memberships—they are actually in a much more fragile position than the person earning $75,000 who only spends $50,000. The high earner has a “burn rate” that leaves almost no room for error. If their industry shifts or their income takes a 10% hit, their entire world collapses. This is why being rich is often described as a performance; it requires a constant stream of new money to keep the lights on and the image intact.

The Role of Lifestyle Inflation and Debt

A major component of the “rich” mindset is Lifestyle Inflation (also known as lifestyle creep). This occurs when every increase in income is immediately met with an increase in spending. Instead of using a raise to build a safety net, the individual upgrades their lifestyle—a better car, a bigger house, or more expensive vacations. Over time, this erodes the possibility of achieving true financial security. Furthermore, many people who appear “rich” are heavily leveraged. They use debt as a tool to project an image of wealth. They may have the “wealthy” look, but their balance sheet is littered with liabilities. When comparing financial security vs rich, you’ll find that rich people often use their money to buy things that depreciate, while secure people use their money to buy time and assets that appreciate.

Case Study: The High-Earner Drifter vs. The Strategic Accumulator

- Meet Mark (The “Rich” Earner): Mark earns $350,000 per year as a top-tier consultant. He drives a $120,000 sports car (leased), lives in a penthouse with a $6,000 monthly rent, and spends heavily on travel and dining to keep up with his peers. Mark has less than $15,000 in his savings account because most of his money goes toward debt payments and luxury costs. If Mark lost his job today, he would be in financial ruin within 60 days.

- Meet Sarah (The “Financially Secure” Earner): Sarah earns $110,000 as a project manager. She lives in a modest home with a fixed mortgage and drives a reliable, paid-off vehicle. Sarah has built an emergency fund of $50,000 and has another $200,000 in diversified investments. Her monthly expenses are only $4,000. If Sarah lost her job today, she could live for over four years without changing her lifestyle or earning another dime.

The Verdict: While Mark looks “richer” at a dinner party, Sarah is the one who truly understands the difference between being rich and being financially secure. Sarah has bought herself freedom; Mark has bought himself a high-pressure cage.

Common Signs You Are Pursuing “Rich” Over “Secure”

To help you audit your own path, here are the hallmark traits of someone who is focusing on the appearance of wealth rather than the foundation of security:

- Net Worth Neglect: You know exactly how much you earn every month, but you have no idea what your total net worth (assets minus liabilities) is.

- The “One Paycheck” Fear: You feel a deep sense of anxiety at the thought of a client leaving or a paycheck being delayed by even a week.

- Depreciating Assets: Most of your “wealth” is tied up in items that lose value over time (cars, clothes, electronics) rather than items that grow (stocks, real estate, businesses).

- Status-Driven Spending: You find yourself making purchases based on how they will be perceived by your social circle or colleagues.

Defining Financial Security: The Foundation of Prosperity

If being rich is a performance, then financial security is the stage upon which that performance sits. While wealth is often about the size of your bank account, financial security is about the strength of your financial foundation. It is a state where your basic needs—housing, food, healthcare, and utilities—are guaranteed for a significant period, regardless of whether you continue to work or not. When we examine financial security vs rich, the most striking difference is that security is a defensive strategy designed to protect you from life’s “worst-case scenarios,” whereas richness is often an offensive strategy focused on accumulation and display.

True financial security creates a psychological buffer. It replaces the “fight-or-flight” response often triggered by money issues with a sense of calm. This isn’t just a feeling; it is a mathematical reality. You are financially secure when your assets and safety nets are robust enough to withstand economic downturns, health crises, or job loss without forcing you to liquidate your lifestyle or go into debt. In the debate of financial security vs rich, security is the baseline that everyone should aim for before they ever worry about “getting rich.”

The Three Pillars of Financial Security

To build a truly secure financial life, you must address three specific areas. These are the structural supports that keep your financial house standing during a storm:

- The Emergency Fund (Liquidity): This is the “peace of mind” fund. Most financial experts recommend a minimum of three to six months of expenses (not income) tucked away in a high-yield savings account. This ensures that a broken furnace or a flat tire is a mere inconvenience rather than a financial catastrophe.

- Low-Burn Debt Management: Financial security is impossible if you are drowning in high-interest debt. Secure individuals prioritize paying off “toxic debt” (like credit cards) and keep their “fixed costs” (mortgage, car payments, insurance) to a small percentage of their total income. This low burn rate is what allows them to survive long periods without fresh income.

- Diversified Cash Flow: Relying on a single paycheck is a high-risk strategy. Financial security is bolstered when you have multiple streams of income—be it from a secondary business, rental income, dividend stocks, or even a well-managed trading portfolio. If one stream dries up, the others keep you afloat.

The “Freedom Ladder” of Financial Security

Building security doesn’t happen overnight; it happens in stages. Below is a breakdown of the various levels of security. Notice how none of these levels require you to own a yacht or a mansion; they are entirely focused on your relationship with your expenses.

| Level | Name | Description |

| Level 1 | The Buffer | You have $1,000–$2,000 saved for immediate emergencies. You no longer use credit cards for surprises. |

| Level 2 | The Safety Net | You have 3–6 months of living expenses saved. You can lose your job and be “okay” for a season. |

| Level 3 | Debt Freedom | All high-interest debt is gone. Your only debt, if any, is a low-interest mortgage. |

| Level 4 | Basic Independence | Your passive income or investment returns cover your “survival” costs (rent/food/utilities). |

| Level 5 | Total Security | Your assets cover your entire current lifestyle indefinitely. Work becomes optional. |

The Peace of Mind Factor

The most significant benefit of choosing financial security over being rich is the reduction in “cognitive load.” When you are merely rich, you are often worried about losing what you have. When you are financially secure, you have already planned for the loss. You have insurance, you have cash reserves, and you have a diversified strategy. This allows you to make better long-term decisions. Instead of making desperate moves to “stay rich,” you can make calculated, patient moves to grow your wealth because you aren’t worried about where your next meal is coming from.

“The goal isn’t more money. The goal is living life on your terms.” — Chris Brogan

In the context of the difference between being rich and being financially secure, remember that security is the floor, and wealth is the ceiling. You should never try to build a ceiling until you are certain the floor can hold the weight.

Comparing Financial Security vs. Wealth: A Deep Dive into the Mindset Gap

When evaluating financial security vs rich, many people realize that these two concepts are not mutually exclusive, but they often move in opposite directions during the early stages of one’s journey. Wealth is traditionally defined as the total value of your assets (cash, stocks, real estate, businesses) minus your liabilities. However, in popular culture, “wealth” is often used interchangeably with “rich,” which is where the confusion starts. To find the difference between being rich and being financially secure, you have to look at how a person handles their surplus capital.

A “rich” person uses their surplus to buy higher-status liabilities (the “Big Three”: luxury cars, expensive primary residences, and designer lifestyles). In contrast, a “financially secure” person uses their surplus to buy productive assets that yield more cash flow. This fundamental choice creates a massive gap in how these individuals experience life. While wealth can be loud and flashy, true financial security is often quiet, private, and incredibly sturdy.

Wealth is What You Don’t See

One of the most important concepts to grasp in the financial security vs rich debate is that true wealth is actually the money you haven’t spent. If you see someone driving a $100,000 car, all you know for certain is that they have $100,000 less than they did before they bought the car (or a significant monthly debt obligation).

The Millionaire Next Door—a famous study of America’s wealthy—found that the majority of people with a net worth over $1 million lived in middle-class neighborhoods, drove used or domestic cars, and avoided luxury brands. Their financial security came from their “invisibility.” Because they didn’t spend their money to look rich, they had the capital available to invest and grow their actual wealth.

The Fragility of Richness vs. The Resilience of Security

To understand why security is more valuable than just being rich, we can look at how different financial structures respond to market volatility. Let’s look at the Asset Allocation typical of these two mindsets:

| Asset Category | The “Rich” Portfolio | The “Financially Secure” Portfolio |

| Primary Focus | Consumption (Cars, High-end fashion) | Accumulation (Stocks, Real Estate, Bonds) |

| Cash Reserves | Low (Most cash goes to debt payments) | High (6-12 months of living expenses) |

| Equity/Investments | Narrow/Speculative | Broad/Diversified |

| Fixed Expenses | 70% – 90% of income | 30% – 50% of income |

| Result of Market Dip | Liquidation of assets at a loss to pay bills | Opportunity to buy more assets at a discount |

The Psychological Shift: Mindset Matters

The difference between being rich and being financially secure is also found in the owner’s mindset.

- The Rich Mindset: “How much can I buy with this paycheck?”

- The Secure Mindset: “How much time can I buy with this paycheck?”

When you prioritize financial security, you are essentially buying back your time. You are creating a world where you no longer have to trade your hours for dollars because your assets are doing the work for you. This is why many successful investors use strategies like trend trading or long-term index investing. They aren’t looking for a quick “score” to buy a new watch; they are looking for consistent, rule-based growth that adds another layer of bricks to their financial fortress.

Facts and Statistics on Wealth and Security:

- The Debt Gap: According to various consumer reports, high-income households often carry the highest levels of non-mortgage debt, frequently using credit to bridge the gap between their high income and their even higher expenses.

- The Emergency Gap: A survey by the Federal Reserve has historically shown that a surprising percentage of high-earners would struggle to cover a sudden $400 emergency without selling something or borrowing money.

- The Longevity of Wealth: Statistics show that “new money” (the rich) often disappears within two generations, whereas “secured wealth” (the financially secure) tends to last much longer because it is built on a foundation of education and asset protection rather than spending.

“True wealth is not about having a lot of money; it’s about having a lot of options.” — Unknown

By understanding the difference between being rich and being financially secure, you can stop playing the “comparison game” with your neighbors and start playing the “freedom game” with your future.

How to Shift Your Mindset from “Getting Rich” to “Being Secure”

Making the transition from chasing the “rich” lifestyle to building financial security requires a fundamental rewiring of how you perceive success. Most people spend their lives focused on their Gross Income—the number on their paycheck or the total revenue from their business. However, income is just a tool; it is not the goal. To understand the difference between being rich and being financially secure, you must pivot your focus toward your Net Worth. Your net worth (Assets minus Liabilities) is the only true scorecard of your financial health. A person earning $1 million a year with a zero net worth is merely a high-paid worker, while a person with a $1 million net worth and no job is truly wealthy.

This mindset shift involves moving away from “consumption-based identity” and toward “asset-based identity.” When you have a consumption-based identity, your self-worth is tied to the things you buy. When you have an asset-based identity, your self-worth is tied to the freedom and options your investments provide. By prioritizing financial security vs rich, you begin to value a growing brokerage account more than a new car, and you start to see every dollar as a “financial soldier” that can go out and work to bring more dollars back to you.

The Art of Intentional Spending

Building security doesn’t mean living a life of extreme deprivation or “pinching pennies” until it hurts. Instead, it involves Intentional Spending. This is the practice of spending extravagantly on the things that truly bring you value while cutting costs mercilessly on the things that don’t. A rich person spends to impress; a financially secure person spends to satisfy.

- Value-Based Budgeting: Instead of a restrictive budget, create a “spending plan” that allocates money to your “Security Bucket” (investments and savings) first, and then allows you to enjoy the rest without guilt.

- The 24-Hour Rule: For any non-essential purchase over a certain amount (e.g., $100), wait 24 hours. This simple pause often breaks the “dopamine loop” of impulsive, rich-seeking behavior.

- The Maintenance Cost Audit: Before buying an asset, calculate its “true cost.” A luxury car doesn’t just cost the sticker price; it costs the higher insurance, premium fuel, and specialized maintenance. Secure individuals look at the Long-Term Cost of Ownership.

Integrating Strategy: Trend Trading for Security

For those who use active strategies like trend trading, the mindset shift is even more critical. In the world of trading, it is easy to get caught up in the “big win” mindset—the desire to get rich quickly on a single trade. However, the difference between being rich and being financially secure in trading is found in your Risk Management.

A trader seeking to “get rich” might over-leverage their account, risking a total wipeout for the chance of a massive payout. A trader seeking “financial security” uses trend trading as a systematic way to grow their capital over time. They understand that the goal of trading is to generate a surplus that can then be moved into “boring,” secure assets like index funds or real estate. This is often called the Core and Satellite strategy. An example:

- The Core (Security): 70% of your wealth is in low-risk, diversified assets that provide the foundation of your security.

- The Satellite (Growth): 30% of your capital is used for higher-performance strategies, like trend trading, to accelerate your growth without ever risking your primary security.

Strategic Planning for the Long Term

True security requires looking past next month and into the next decade. This is where Strategic Planning comes into play. When comparing financial security vs rich, security is often the result of being “boringly consistent” with the following:

- Tax Optimization: Understanding how to keep more of what you earn through legal tax-advantaged accounts (like 401ks, IRAs, or HSAs).

- Inflation Protection: Ensuring your security isn’t eroded by the rising cost of living. This means investing in assets that historically outpace inflation, such as equities or real estate.

- Legacy and Estate Planning: Security isn’t just for you; it’s for your family. Having a will, a trust, and proper insurance ensures that your security survives even if you aren’t there to manage it.

“The individual who is financially secure has a level of independence that the ‘rich’ person who is slave to their debt can never know.”

Practical Steps to Build Your Own Financial Fortress

Transitioning from a lifestyle focused on the appearance of success to one anchored in reality requires a tactical approach. Building a “financial fortress” is the process of creating a system that prioritizes financial security vs rich. This isn’t about one-off wins or “getting lucky” in the market; it is about building a structural defense that makes your financial survival independent of outside forces. By following a specific set of practical steps, you can widen the difference between being rich and being financially secure in your own life, moving away from high-stress “richness” and toward durable stability.

Audit Your Cash Flow and Lower Your “Burn Rate”

The first step in building security is knowing exactly where your money goes. Most people who focus on “being rich” only look at their income. To be financially secure, you must look at your Burn Rate—the total amount of money you spend each month to maintain your life. The lower your burn rate, the easier it is to achieve security. If you earn $10,000 but spend $9,500, you are financially fragile. If you earn $6,000 but spend $3,000, you are building a fortress.

- Fixed vs. Variable Costs: Categorize your spending. Fixed costs (rent, insurance, debt) should ideally stay below 50% of your take-home pay.

- The “Luxury Audit”: Identify expenses that are strictly for “status” and evaluate if they actually provide a return on happiness.

- Targeting the Gap: Your goal is to increase the “Gap”—the difference between what you earn and what you spend. This gap is the raw material used to build your security.

Building an “Unshakeable” Foundation through Automation

One of the most effective ways to ensure you choose financial security over wealth is to take human emotion out of the equation. Humans are biologically wired to spend what they see. By automating your finances, you ensure that your security is built before you ever have the chance to spend your paycheck on “rich” status symbols.

- Automated Savings: Set up a direct transfer from your paycheck to a high-yield emergency fund.

- Automated Investing: Schedule monthly contributions to diversified index funds or your trading account.

- The “Tax-First” Rule: Ensure your retirement contributions (401k/IRA) are deducted before the money hits your bank account.

Risk Management: Protecting the Fortress

A fortress isn’t just about thick walls; it’s about having a plan for when things go wrong. In the world of financial security vs rich, risk management is what separates the survivors from those who go bust. Whether you are a long-term investor or someone who uses trend trading to grow their capital, you must protect your downside.

- Insurance as a Shield: Ensure you have adequate health, disability, and life insurance. These are the “moats” around your fortress that prevent a single accident from draining your life’s savings.

- The “Stop-Loss” Mindset: Just as a disciplined trend trader uses stop-loss orders to prevent a single bad trade from ruining their account, a secure individual uses “life stop-losses.” This means having a plan for when to cut expenses or pivot careers if a specific income stream starts to trend downward.

- Asset Protection: As your net worth grows, consider how to shield your assets from liability or legal issues through proper entity structuring or umbrella insurance.

The Marathon Mindset: Consistency as a Strategy

The final practical step is acknowledging that the difference between being rich and being financially secure is often a matter of time. Looking rich can happen overnight (through debt or a windfall), but becoming secure is a marathon. It requires the discipline to stay the course even when it’s not “exciting.”

Case Study: The Tale of Two Portfolios (2020–2026)

Consider two individuals during a period of market volatility:

- The “Rich” Speculator: Focused on high-growth, high-risk assets to double their money quickly. When the market corrected, they had no cash reserves and were forced to sell their “status” assets (cars, watches) at a 40% loss just to pay their mortgage.

- The “Secure” Strategist: Used a trend trading approach for a portion of their portfolio but kept 60% in stable, liquid assets. When the market dipped, they didn’t just survive; they had the cash on hand to buy more assets at a discount.

| Strategy Component | Speculator (Rich-Seeking) | Strategist (Security-Seeking) |

| Emergency Fund | None ($0) | 12 Months ($60,000) |

| Reaction to Market Dip | Panic and Liquidation | Patience and Execution |

| Debt Usage | High (Consumer Debt) | Low (Strategic/Mortgage only) |

| 2026 Outcome | Starting over from zero | Net worth increased by 25% |

Frequently Asked Questions (FAQ)

To wrap up our deep dive into the difference between being rich and being financially secure, we’ve compiled answers to the most common questions readers have when navigating the path between status and stability.

Is it better to be rich or financially secure?

Most people assume they have to choose, but the ideal goal is to become financially secure first. Once you have a bedrock of security—where your basic life costs are covered and you have a substantial buffer—you can then safely pursue “wealth” (a higher net worth) without the anxiety of losing everything. Think of security as your foundation and wealth as the structure you build on top of it. You wouldn’t build a mansion on a swampy, unstable foundation; don’t try to build massive wealth on a foundation of debt and paycheck-to-paycheck living.

Can you be both rich and financially secure?

Absolutely. In fact, many people who are truly wealthy are also incredibly secure. The difference is the order of operations. A person who is both wealthy and secure has mastered their cash flow, minimized their “burn rate,” and accumulated assets that generate passive income. They could live a flashy, “rich” lifestyle, but they choose not to because they value their financial freedom more than the temporary status that “being rich” provides.

How much money do I need to be financially secure?

There is no magic number because security is relative to your Burn Rate. Use this simple formula:

Monthly Survival Cost × 6 (Months of Emergency Fund) = Baseline Security

If your basic survival costs (housing, food, utilities, insurance) are $3,000 per month, an $18,000 liquid emergency fund is your first major milestone toward security. Once you have that, you are technically more secure than the majority of the population.

Does paying off debt make me more secure?

Yes, it is arguably the most effective way to improve your security. Every dollar you spend on interest is a dollar that isn’t working for your future. When you pay off a debt, you permanently lower your “burn rate,” which makes you more resilient to job loss or income changes. Debt freedom is the ultimate form of financial security.

How do I start if I’m currently living paycheck to paycheck?

Start by focusing on the Gap. Even if you can only save $50 a month, you are building the habit. Once that habit is formed, look for ways to increase your income (side hustles, career moves) while keeping your expenses flat. The extra money you earn should go 100% into your “Security Bucket” until your foundation is rock solid.

Conclusion: Redefining Success

The difference between being rich and being financially secure comes down to one fundamental concept: control.

When you focus on “being rich,” you are often at the mercy of your income, your creditors, and the opinions of others. You are performing for an audience that doesn’t actually care about your long-term well-being. But when you prioritize financial security vs rich, you take back control. You are no longer worried about the next economic downturn because you have built a life that can withstand it.

True success isn’t defined by the car you drive or the size of your house. It is defined by the freedom to wake up every morning and choose how you spend your time. It is the ability to walk away from a toxic job, to help a loved one in need without panic, and to invest in your future with confidence.

Final Call to Action:

Financial security is not a destination you reach; it is a way of living. Don’t wait for a “big break” to get started. Audit your finances today, calculate your freedom number, and take one small, intentional step toward your own financial fortress. Which one are you building today: a performance for others, or a future for yourself?

If you enjoyed this deep dive, learn how to use leverage for long-term trend trading to accelerate your journey to total financial independence. Find out more about The SS Capital Group